Traders work on the floor of the London Metal Exchange in London, Britain, September 27, 2018. REUTERS/Simon Dawson//File Photo

LONDON, Nov 12 (Reuters) - What happens when the market of last resort, the London Metal Exchange (LME), runs out of metal? And should it then restrict the right to take metal out of its warehouses if the result is price distortion?

The 144-year old exchange, which sets benchmark prices for the global industrial metal markets, has always prided itself on its role as ultimate buyer and ultimate seller of physical metal.

But "there's a fascinating policy question" of whether that should always be the case, LME chief executive Matthew Chamberlain told the Reuters Commodities Summit.

Chamberlain's musings come after the LME was forced to restrain its copper contract, which risked a disorderly breakdown after on-warrant exchange stocks slumped to a multi-decade low of 14,150 tonnes.

They have since rebuilt to 49,900 tonnes but it's not just a copper problem. LME tin stocks have been at super-low levels for most of the year. Lead stocks are looking similarly depleted. Backwardation has become entrenched in both contracts' forward curve.

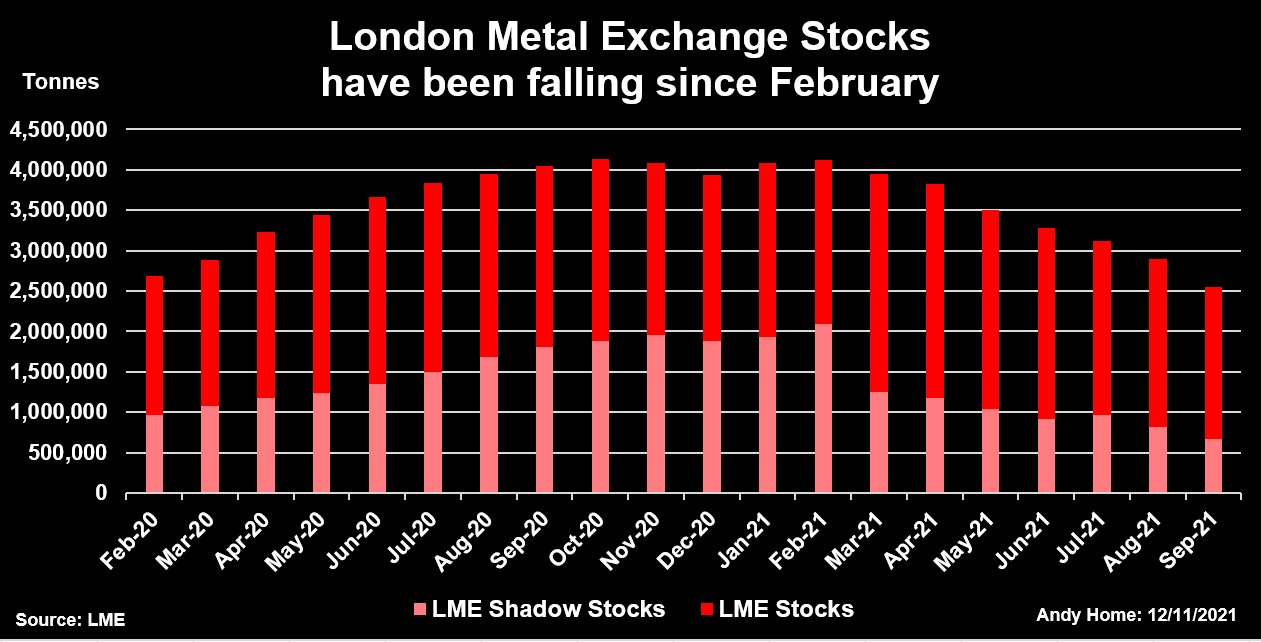

Indeed, total registered LME inventory has fallen by almost 600,000 tonnes since the start of the year. Stocks of all metals stand at 1.469 million tonnes, the lowest since 2008.

The visible draws have been complemented by an even bigger reduction in LME shadow stocks, which slumped by 64%, or 1.21 million tonnes, over the first nine months of 2021.

CHANGING FUNDAMENTALS

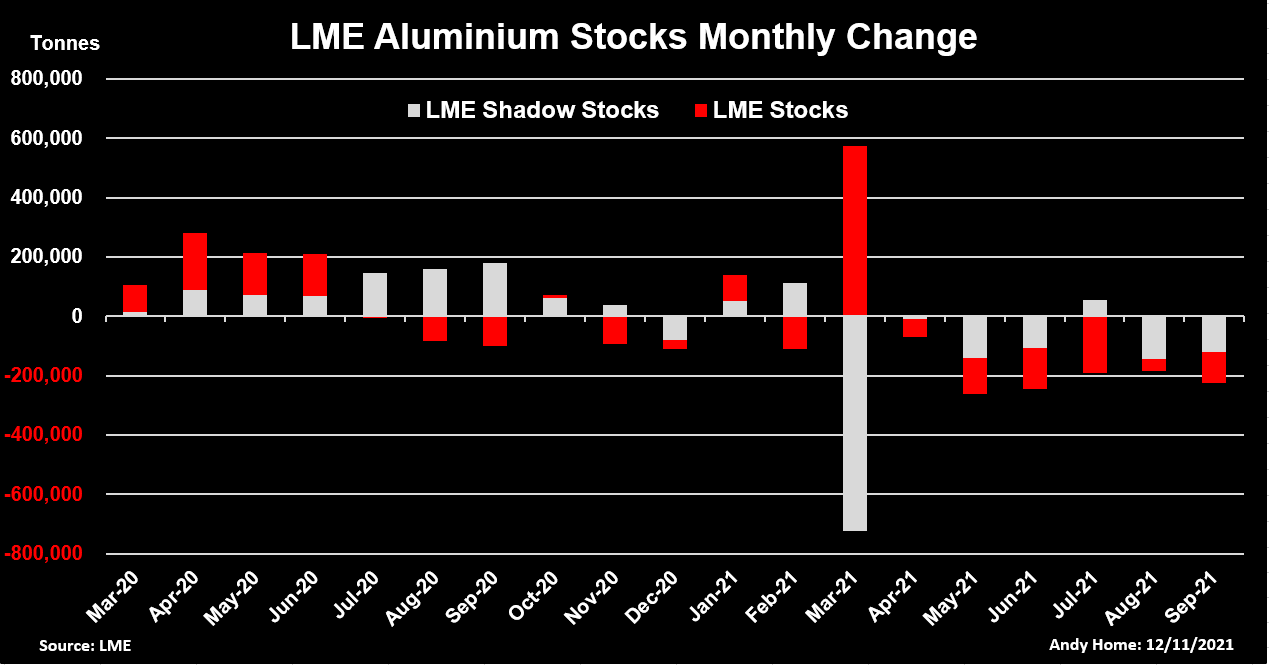

The largest component of LME inventory has historically been aluminium, a market until recently notable for excess global production capacity and high stocks.

Fierce competition for low-cost storage has characterised the LME aluminium market for over a decade. A lot of metal rotates between on-warrant and LME shadow storage, defined as a warehousing deal with explicit reference to the option of LME delivery.

March saw a particularly large turn of the storage wheel with shadow stocks slumping by 723,000 tonnes and LME registered stocks surging by 557,000 tonnes.

However, stocks in both categories have since fallen in tandem. Shadow aluminium inventory was 558,548 tonnes at the end of September, down from a high of 1.74 million tonnes in February and the lowest level since the exchange started publishing its monthly reports in February 2020.

Combined on- and off-warrant inventory fell by 1.13 million tonnes over January-September and a lot more metal has left the on-exchange tally since then.

The seepage of so much aluminium away from the LME warehousing network attests to the turnaround in the market's fundamentals, particularly the emergence of China as a major importer of commodity-grade metal due to energy-related production closures.

LME inventory is being used to plug supply gaps that have opened up elsewhere which is how the market of last resort is supposed to work.

SHIPPING PROBLEMS

The strength of the post-COVID manufacturing recovery, first in China and now in the rest of the world, has impacted not just aluminium but all of the LME metals to varying extents.

Supply-chains, by contrast, are stressed by continued disruption in the global shipping sector, where container rates remain high and many ports, particularly U.S. ones, log-jammed.

This has generated an additional call on LME stocks, lead being the clearest example.

Registered LME lead inventory of 53,700 tonnes is down by 60% on the start of the year and close to last month's multi-year low of 48,175 tonnes.

Stocks in Europe, where supply has been hit by the outage of Germany's Stolberg smelter, have fallen particularly sharply and are still draining away. European locations hold just 12,325 tonnes with a minimal 234 tonnes sitting in shadow storage at the end of September.

There is no lead at all at U.S. locations, which is underpinning historically high physical premiums.

There is plenty of lead sitting in Shanghai. Under other circumstances it would have surged towards the nearest LME warehouses in Taiwan or South Korea in response to the cash premium.

China's exports picked up noticeably in September and a total 9,400 tonnes were delivered into LME warehouses in those countries in the middle of October. But arrivals have since slowed to a trickle, suggesting that high shipment costs are constricting the anticipated arbitrage flow.

With supply scarce in both U.S. and European markets, it's clear that LME lead stocks won't recover until shipping rates normalise.

OUT OF STOCK

Resurgent demand, production problems and shipping constraints have already depleted LME stocks of tin.

They've been super-low all year and currently total a minimal 845 tonnes with 155 tonnes earmarked for physical load-out. Shadow stocks at the end of September were just 50 tonnes.

While a reflection of tin's current dynamics, such low inventory leaves the market extraordinarily vulnerable to potential distortion.

You could buy the remaining LME open tonnage for $26 million, at which stage you'd have cornered the market.

The exchange almost certainly wouldn't allow that to happen although it has tolerated the cancellation of 180,000 tonnes of copper over a four-week window, which resulted in the most ferocious backwardations in living memory.

Shadow stocks of copper were just 28,828 tonnes at the end of September, meaning low availability of immediately-warrantable metal going into the October tightness.

Moreover, the ability of shorts more generally to deliver metal against the cash premium has also been restricted by the multiple global logistics bottle-necks.

With hindsight. the LME contract was as vulnerable as tin to the mass removal of stocks, which is why the exchange had to step in and cap lending rates.

Those "special measures" remain in place and will do so until inventory rebuilds to a point that spreads won't immediately go wild again as soon as the restraints are off.

There's been a conspicuous absence of fresh copper stock cancellation activity since the LME intervened but at some stage someone's going to need metal from exchange warehouses again.

Will there be enough copper at that stage to avoid another time-spread crunch? The broader cross-metals picture of declining LME inventory suggests not.

You can start to understand why the LME's Chamberlain is questioning the limits of being a market of last resort.

The opinions expressed here are those of the author, a columnist for Reuters.

Editing by Barbara Lewis

Our Standards: The Thomson Reuters Trust Principles.

"exchange" - Google News

November 12, 2021 at 11:10PM

https://ift.tt/30dyBU6

Column: Falling stocks pose problems for London Metal Exchange - Reuters

"exchange" - Google News

https://ift.tt/3c55nbe

https://ift.tt/3b2gZKy

Exchange

Bagikan Berita Ini

0 Response to "Column: Falling stocks pose problems for London Metal Exchange - Reuters"

Post a Comment